Piece rate wages are paid based on the number of units produced; for example, if the piece rate wage is $4 per unit and a worker produces 10 units, then the total piece rate wage is $40. Gross margin is the difference between revenue and the cost of goods sold (COGS). On the other hand, contribution margin refers to the difference between revenue and variable costs. At the same time, both measures help analyze a company’s financial performance. Contribution margin analysis is the gain or profit that the company generates from the sale of one unit of goods or services after deducting the variable cost of production from it. The calculation assesses how the growth in sales and profits are linked to each other in a business.

Some other helpful tools for business

Since machine and software costs are often depreciated or amortized, these costs tend to be the same or fixed, no matter the level of activity within a given relevant range. That is, fixed costs remain unaffected even if there is no production during a particular period. Fixed costs are used in the break even analysis to determine the price and the level of production.

Fixed Cost vs. Variable Cost

This concept is especially helpful to management in calculating the breakeven point for a department or a product line. Management uses this metric to understand what price they are able to charge for a product without losing money as production increases and scale continues. It what are real estate transfer taxes also helps management understand which products and operations are profitable and which lines or departments need to be discontinued or closed. Yes, it means there is more money left over after paying variable costs for paying fixed costs and eventually contributing to profits.

Is a high contribution margin ratio good?

Contribution margin, gross margin, and profit are different profitability measures of revenues over costs. Gross margin is shown on the income statement as revenues minus cost of goods sold (COGS), which includes both variable and allocated fixed overhead costs. Profit is gross margin minus the remaining expenses, aka net income.

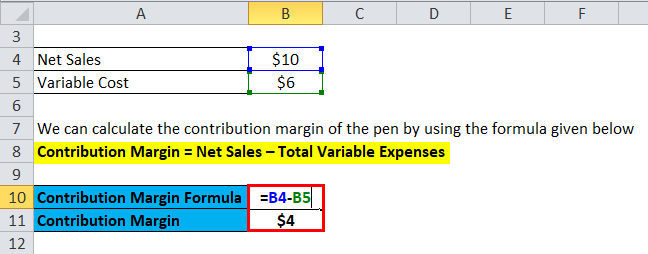

How to calculate contribution margin

- It also helps management understand which products and operations are profitable and which lines or departments need to be discontinued or closed.

- The contribution margin ratio (CMR) expresses the contribution margin as a percentage of revenues.

- The concept of contribution margin is applicable at various levels of manufacturing, business segments, and products.

- For each type of service revenue, you can analyze service revenue minus variable costs relating to that type of service revenue to calculate the contribution margin for services in more detail.

In short, profit margin gives you a general idea of how well a business is doing, while contribution margin helps you pinpoint which products are the most profitable. The best contribution margin is 100%, so the closer the contribution margin is to 100%, the better. The higher the number, the better a company is at covering its overhead costs with money on hand. The contribution margin ratio is calculated as (Revenue – Variable Costs) / Revenue. Investors examine contribution margins to determine if a company is using its revenue effectively.

You can use it to learn how to calculate contribution margin, provided you know the selling price per unit, the variable cost per unit, and the number of units you produce. The calculator will not only calculate the margin itself but will also return the contribution margin ratio. For the month of April, sales from the Blue Jay Model contributed \(\$36,000\) toward fixed costs.

Say, your business manufactures 100 units of umbrellas incurring a total variable cost of $500. Accordingly, the Contribution Margin Per Unit of Umbrella would be as follows. This means that the production of grapple grommets produce enough revenue to cover the fixed costs and still leave Casey with a profit of $45,000 at the end of the year. The concept of this equation relies on the difference between fixed and variable costs. Fixed costs are production costs that remain the same as production efforts increase.

The contribution margin ratio (CMR) expresses the contribution margin as a percentage of revenues. In May, 750 of the Blue Jay models were sold as shown on the contribution margin income statement. When comparing the two statements, take note of what changed and what remained the same from April to May. For example, raising prices increases contribution margin in the short term, but it could also lead to lower sales volume in the long run if buyers are unhappy about it.

When the contribution margin is calculated on a per unit basis, it is referred to as the contribution margin per unit or unit contribution margin. You can find the contribution margin per unit using the equation shown below. For example, assume that the students are going to lease vans from their university’s motor pool to drive to their conference. A university van will hold eight passengers, at a cost of $200 per van.

In our example, if the students sold \(100\) shirts, assuming an individual variable cost per shirt of \(\$10\), the total variable costs would be \(\$1,000\) (\(100 × \$10\)). If they sold \(250\) shirts, again assuming an individual variable cost per shirt of \(\$10\), then the total variable costs would \(\$2,500 (250 × \$10)\). In the Dobson Books Company example, the total variable costs of selling $200,000 worth of books were $80,000. Remember, the per-unit variable cost of producing a single unit of your product in a particular production schedule remains constant.